How to Decide When to Start Taking Social Security

Many affluent investors have not fully considered how their Social Security benefit will affect their overall financial plan. Although Social Security was created during the Great Depression as a retirement safety net, benefits now cover an estimated 96% of Americans.

Today, Social Security benefits make up an average of 40% of a typical retiree’s income. Because your Social Security benefit is calculated using your earned income throughout your career, the income can be significant, even for wealthy retirees.

Some points to consider, covered in more detail below:

- Your Social Security benefit amount can make a significant impact on your total retirement income, with the total maximum value of lifetime Social Security payments is estimated to be about $572,000 for men and $683,000 for women.

- The timing of when you choose to collect these benefits will impact the amount of benefit you receive.

- Your online Social Security account can provide you with pertinent information about your future benefits to help you decide when to claim.

- Working while receiving benefits can have an effect on your taxes and ongoing benefit amount.

Is Social Security Enough to Make an Impact?

While the average Social Security retirement benefit payment is about $1,342 per month, the maximum benefit at full retirement age for 2017 is $2,687 per month. For those who wait until age 70 to start receiving payments, the maximum monthly payment for 2017 is $3,538.

Because Social Security payments are increased with Cost of Living Adjustments, the monthly benefit will continue to grow throughout your retirement. Even if you don’t need Social Security payments to live on during retirement, the benefits can be invested or gifted to your heirs.

For someone who has reached full retirement age with an average life expectancy, the total maximum value of lifetime Social Security payments is estimated to be about $572,000 for men and $683,000 for women, according to SSA.gov. It’s important to plan ahead to maximize your total lifetime benefit and plan to use the asset as part of your overall financial plan.

When Should You Start Taking Social Security?

Social Security benefits can be claimed anytime between ages 62 and 70. However, the timing of when you choose to collect these benefits will impact the amount of benefit you receive.

Early Retirement

If you choose or are forced into an early retirement, you can begin receiving Social Security benefits as early as age 62. However, if you file to receive benefits any time before reaching your full retirement age, you will receive a reduced benefit. Your basic benefit is reduced a fraction of a percent for each month you begin receiving benefits prior to full retirement age, up to 30%.

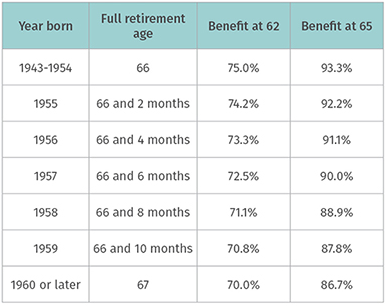

Full Retirement Age

Full retirement age (FRA) changes based on the year you were born. For those born in 1937 and earlier, FRA is 65. After 1937, two months is added each year until FRA becomes 66 for those born between 1943 and 1954. Starting in 1955, two months a year is added again until the FRA becomes 67 for those born in 1960 or later.

If you wait until you reach full retirement age to begin collecting your social security benefits, you will receive your full Primary Insurance Amount, which is the full benefit that you have earned.

Delayed Benefits

If you continue working past your FRA or you don’t need your social security benefit to live on, you can delay receiving your benefits. For each year that you delay, your benefit will increase 8%, for a maximum possible increase of 32%. Your benefit is only increased until you begin receiving it or you turn 70, whichever happens first.

What If I Want To Keep Working?

If you have already started receiving Social Security benefits but want to keep working, there are a few pieces of information you must keep in mind. First, your benefit might be increased or decreased, depending on your income. If you earned more in the past year than one of the years used to calculate your benefit, you will receive an increased amount going forward.

On the other hand, you could experience a reduction in your benefits based on the following information:

- If you are younger than FRA and make more than $16,920 (for 2017), the SSA will deduct $1 from your benefits for every $2 you earn above that amount.

- In the year you reach FRA, they will take out $1 for every $3 you earn above $44,880.

- If you are already at FRA, your earnings will not make a difference in your benefits.

If you want to see how working while receiving Social Security will affect your benefits, use this calculator.

Now let’s talk taxes. Working once you’ve started receiving benefits can cause some tax confusion. The SSA uses your combined income to determine if you need to pay taxes on the benefits you receive. They calculate this total as follows: your adjusted gross income + nontaxable interest + ½ of your Social Security benefits.

If you are a single-filer and your combined income is between $25,000 and $34,000, you may be required to pay tax on up to 50% of your benefits, and if you made more than $34,000, you will pay up to 85%. If you file jointly, you may have to pay up to 50% on $32,000-$44,000 and 85% if it’s in excess of $44,000.

When is the Optimal Time to Begin Collecting Benefits?

By the time most retirees are making this decision, it is too late to change how much they pay into the system, so the only control they have over the amount of their benefit is how early or late they decide to file and claim it.

Social Security Statement

The first step in deciding when to begin collecting Social Security is to gather pertinent information. You can register for a “my Social Security” account which allows you to view estimates for your monthly benefit if taken at age 62, your full retirement age, or the maximum benefit at age 70. It also contains estimates of disability, family, and survivor benefits as well as Medicare information. The amounts listed are only estimates and are subject to change. They are calculated based on your date of birth and future estimated taxable earnings. The Social Security Administration also offers the option of receiving your statement by mail, if that’s what you would prefer.

You will also be able to view your earnings history through your online account. It is important to review this information for errors and compare it to your tax return annually because this is what your benefit amount is based upon. The SSA can make mistakes on your earnings register, and it is much easier to correct them right away then waiting until you are 70. This is especially important information for those who have spent some time out of the workforce, whether to raise a family, disability, or other reasons. As benefits are calculated based on the top 35 years’ earnings, it may be worthwhile to work a few more years if you find yourself with just shy of 35 years’ worth of wages.

Deciding When to Claim Benefits

Social Security benefits are calculated using complex actuarial equations based on life expectancy and estimated rates of return. They are not designed to encourage early or late retirement; based on the calculations the total amount you receive over your lifetime should be about the same whether you claim it at age 62 or 70. You either receive the money as a smaller monthly payment over a longer period of time or a larger monthly payment over a shorter period of time.

Deciding on the best time for you to claim your benefits depends upon how you compare to the averages. As of today, a man turning 65 is expected to live until age 84.3 and a woman of 65 until age 86.6. If based on your health and your family history of longevity, you believe you will live much longer than that, your overall lifetime benefit will be greater if you delay claiming your benefits to increase your benefit amount. If the opposite is true, and you see little chance of making it into your mid 80’s, you would receive a greater lifetime benefit by taking it sooner, even though it is a lower monthly payment.

Aside from life expectancy, rates of return must also be taken into consideration. Social Security growth is calculated at the Treasury-bond rate. If you are able to invest your benefit instead of spending it, you may be better off claiming early and investing it in an effort to earn better rates of return. In this way, though you start with a smaller monthly payment, the growth from your investments may leave you with more money than if you had waited to receive the Social Security Administration’s increased payment.

Once you decide the best time to retire and begin collecting benefits, it is important to remember to complete your application for Social Security benefits three months before the month in which you want your retirement benefits to begin. If you think you need extra assistance, you can contact the SSA for counseling. If you decide to go this route, make sure that you keep copious notes about your meeting, including dates and names. To ensure you are getting correct and unbiased information, speak to at least two different employees, asking them the same questions. Consider consulting with a senior advisor instead.

To learn more about optimizing your total Social Security benefit, it’s best to speak with an experienced financial professional about your specific situation. If you have questions about your Social Security strategy, call our office today at 1-866-587-1230 or email me today at todd@frankfinancial.net

Do You Have Important

FINANCIAL QUESTIONS?

Accept our offer of a free

Financial Planning Checkup

Todd E. Frank, CPA/PFS, MBA is the President and CEO of Frank Financial Advisors, a Registered Investment Advisory Firm (RIA) serving clients nationwide from our headquarters in Carlsbad, San Diego, California. As an RIA, Frank Financial Advisors is able to offer truly independent, fee-only financial advisory services.

Todd E. Frank, CPA/PFS, MBA is the President and CEO of Frank Financial Advisors, a Registered Investment Advisory Firm (RIA) serving clients nationwide from our headquarters in Carlsbad, San Diego, California. As an RIA, Frank Financial Advisors is able to offer truly independent, fee-only financial advisory services.